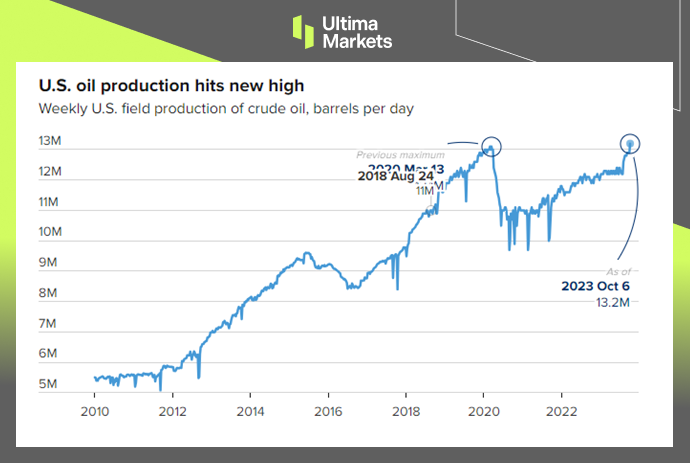

U.S. oil production hits record high

The U.S. Department of Energy announced on Oct. 12 that U.S. crude oil production had hit an all-time high of 13.2 million barrels per day, entirely wiping out Covid-era losses of more than 3 million barrels per day. Meanwhile, the S&P 500 Energy Index tripled after three and a half years.

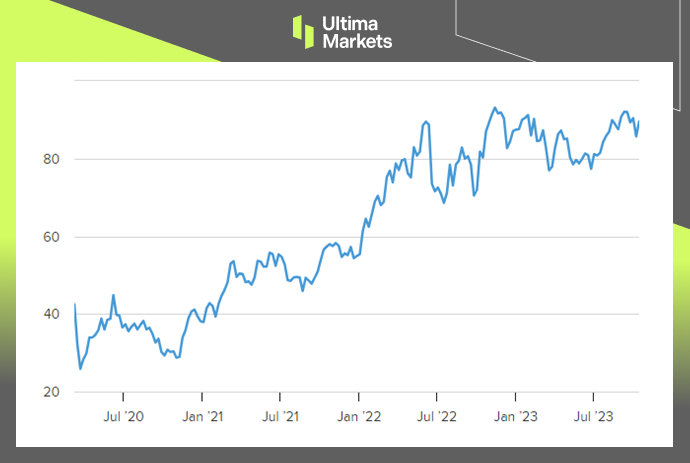

Oil demand has slowly rebounded after the 2020 downturn and lingering supply-chain shock. And rising prices for WTI crude – which careened during Covid to less than $15 a barrel, shot back to $120 in 2022, and is now near $90 – can make previously unprofitable plays work.

(US oil production,Energy Information Administration)

Oil companies conservative in capital spending

U.S. oil companies cut capital spending to $106.6 billion last year from $199.7 billion in 2014, according to Statista, contributing to the decline in oil production and arguably delaying the recovery. And they put that money to work paying higher dividends and doing stock buybacks.

According to Energy Department data, oil and gas companies paid about $75 billion per quarter last year. The department says the share of oil-company operating cash flow going to shareholders rose to half of operating cash flow from about 20% in 2019.

(S&P Energy Sector Index)

Higher productivity per crude well

Offsetting the decline in capital spending is higher productivity per well — while all of the U.S. oil production is back, the closely watched Baker-Hughes rig count is barely half of 2018 levels. The average production per rig of new wells just topped 1,000 barrels a day, up from 668 four years ago, according to the Energy Department. So the industry didn’t have to add a ton of new wells or drill in as many new places to recover fully.

Even as more cars go electric, demand from older cars and uses of oil in chemicals will keep the oil business very large. “The U.S. production will rise to 13.6 million barrels per day next year and 13.9 million in 2025. After that, forecasts get more difficult because so much can change, but by late this decade oil consumption should peak before beginning to ebb”, Rystad Energy said.

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.