China Expected to Lift Procurement Ban during APEC

On Nov. 13th, the Dubai Airshow commenced, and Boeing (BA.US), the jet manufacturer of Dow Jones, has already successfully secured a series of significant orders. Emirates has agreed to acquire 90 Boeing 777 aircraft, which are valued at an impressive $52 billion. Additionally, Emirates’ sister airline, Flydubai, will be incorporating 30 Boeing 787 Dreamliners into its fleet through an $11 billion agreement. This significant deal arrives at a time when Emirates is looking to enhance its aircraft portfolio.

Separately, SunExpress, a joint venture between Turkish Airlines and Lufthansa, also announced a major order for Boeing 737 aircraft. The deal includes an order for 28 737-8 models and 17 737-10 models, with the option to purchase up to 45 additional 737 MAX planes. SunExpress has previously placed an order for 42 737-8 aircraft, of which nine have already been delivered. Furthermore, Ethiopian Airlines finally announced that it has decided to resume flying the 737 MAX after the 2019 crash incident. Ethiopian Airlines revealed on Tuesday that it has agreed to a deal with Boeing for the purchase of 20 737 MAX planes and 11 more 787 Dreamliners. Boeing stated that the sale was the largest-ever purchase of its airplanes in African history, however, declined to disclose the value of the deal.

According to reports, China is considering lifting a sales freeze on Boeing 737 Max jets, potentially paving the way for the planemaker to resume sales in the country. The news comes as President Biden and President Xi are set to meet at the APEC conference in San Francisco, raising the possibility that the sales freeze could be lifted in conjunction with the meeting. While China is reportedly considering a commitment to purchase 737 jets, discussions are still underway and President Xi is not expected to announce a formal order. If this move comes to fruition, it would be a major development for Boeing, which hasn’t made significant sales in China since 2018 following the grounding of the 737 Max after two crashes. After receiving a string of positive updates, Boeing experienced two consecutive days of trading gains.

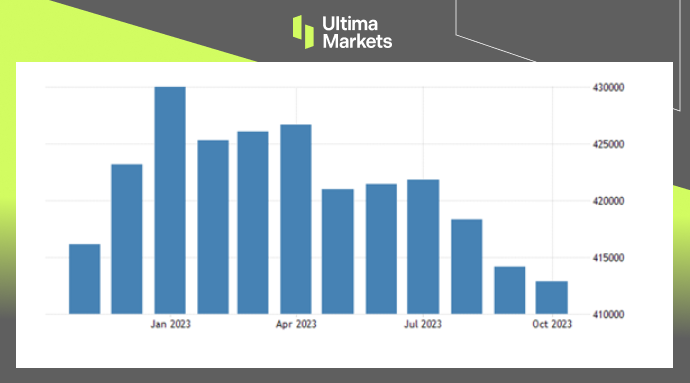

(Boeing Stock Performance Six-month Chart)

Disclaimer

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.